The return on each new dollar of US debt is plummeting to new lows according to figures from the Federal Reserve.

The return on each new dollar of US debt is plummeting to new lows according to figures from the Federal Reserve.

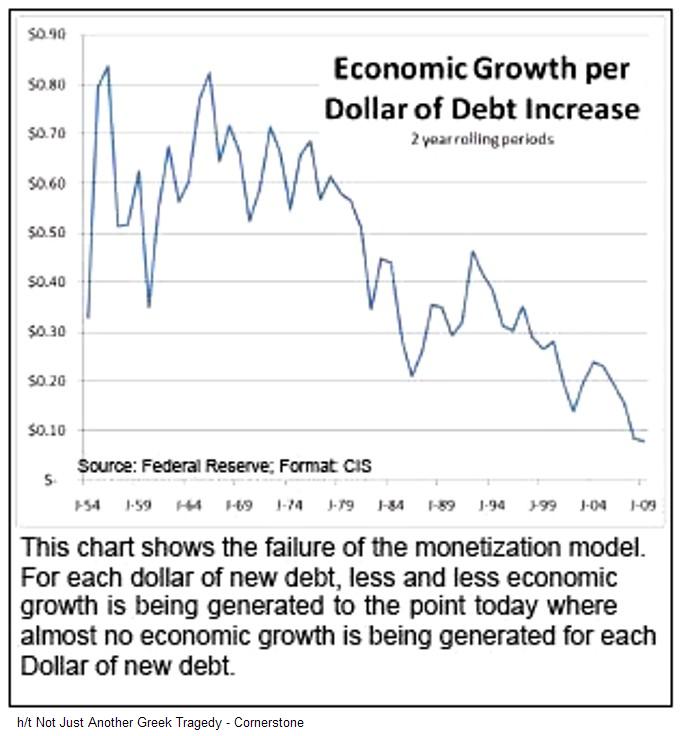

The chart below is from the essay, Not Just Another Greek Tragedy by Cornerstone.

I have been watching this chart for the past ten years, as part of the dynamic of the sustainability of the bond and the dollar as the limiting factor on the Fed's ability to expand the money supply.

The ability to expand debt is contingent on the ability to service debt. If the cost of the debt rises over the net income of the country's capital investment, or even gets close to it, the currency issuing entity is trapped in a debt spiral to default without a radical reform.

In other words, if each new dollar of debt costs ten percent in interest, largely paid to external entities, and it generates less than ten cents in domestic product, it is a difficult task to grow your way out of that debt without a default or dramatic restructuring.

So we are not quite there yet. But we are getting rather close on an historic basis. Without the implicit subsidy of the dollar as the world's reserve currency it would be much closer.

As it is now, this chart indicates that stagflation at least, rather than a hyperinflation, is in the cards for the US. But the trend is not promising, and the lack of meaningful reform is devastating.

A 'soft default' through inflation is the choice of those countries that have the latitude to inflate their currencies. Greece, being part of the European Monetary Union, did not. The US is not so constrained, especially since it owns the world's reserve currency.

The economy is out of balance, heavily weighted to a service sector, especially the financial sector which creates no new wealth, but merely transforms and transfers it. With stagnation in the median wage, and an historic imbalance in income distribution skewed to the top few percent, with the banks levying de facto taxation and inefficiency on the economy as a function of that income transfer, there should be little wonder that the growth of real GDP is sluggish in relation to new debt.

Or as Joe Klein so colorfully phrased it, the elite have been strip-mining the middle class in America for the past thirty years.

Along with the 'efficient market hypothesis,' trickle-down economics is also a fallacy. This is why the stimulus program being conducted by the Federal Reserve, in an egregious expansion of its authority to conduct monetary policy, in subsidies and transfer payments to Wall Street is not working to stimulate the real economy. It merely inflates the bonuses of the few, and extends the unsustainable.

So obviously one might say, "The Banks must be restrained, and the financial system reform, and the economy brought back into balance, before there can be any sustained recovery.

11 May 2010

Here Is Why the Fed Cannot Simply Continue to Inflate Its Way Out of Every Financial Crisis That It Creates

Category:

debt to gdp,

economic imbalances,

economic myths,

financial reform,

stagflation